Homeowners who are considering maximizing their home equity for big-ticket expenses often turn to the HELOC (home equity line of credit) as a flexible financing option. A HELOC works like a credit card, allowing you to borrow against the equity you’ve built up in your home, drawing only what you need and paying interest only on the amount borrowed. But one question always looms: How much HELOC interest will you end up paying?

We wrote this article to explain how much interest you would pay on a $200,000 HELOC at a 7% interest rate. To understand this, we will break down the interest calculation process and offer insights on how HELOCs work, shedding light on factors that influence the total interest paid.

How HELOC Interest Works in 2026

Before diving into the specifics, it’s essential to understand that with a HELOC, you’re not required to take the full loan amount upfront. Instead, you can borrow only what you need, when you need it, up to the maximum approved limit (in this case, $200,000). This is why the interest you pay depends on two key factors: how much you borrow and how long you take to repay it.

Most HELOCs have two distinct periods: the draw period and the repayment period. During the draw period, which typically lasts between 5 and 10 years, you can borrow funds as needed. The HELOC interest during this time is usually calculated on a variable rate basis, and you typically make interest-only payments on the amount borrowed.

After the draw period ends, the repayment period begins, where you’ll need to start paying both principal and interest on the outstanding balance. Why take out a lump-sum loan when you can borrow exactly what you need over time and save on unnecessary interest payments?

How Much Interest Would Be Paid on a $200,000 HELOC at 7%?

Calculating Interest on a $200,000 HELOC at 7%

Let’s assume you’ve been approved for a $200,000 HELOC at a 7% interest rate. The exact interest you’ll pay will depend on how much of the credit line you actually use. For this example, we’ll consider a few different scenarios to give you a sense of how the numbers work.

Scenario 1: Borrowing $100,000

In this scenario, you decide to borrow half of the available credit, or $100,000, during the draw period. The interest is calculated based on the amount you borrow, not the total credit limit. Using the basic interest formula, we can estimate your annual interest payments: Interest=Loan Amount×Interest Rate\text{Interest} = \text{Loan Amount} \times \text{Interest Rate} Interest=100,000×0.07=7,000\text{Interest} = 100,000 \times 0.07 = 7,000In the first year, you would pay $7,000 in interest on the $100,000 borrowed at a 7% rate. If you continue to only make interest payments, you would pay $7,000 each year for as long as the draw period lasts, which could be several years. Keep in mind, during the draw period, your principal remains unpaid unless you choose to make additional payments toward it.

Scenario 2: Borrowing $50,000

Now, let’s say you only use $50,000 of your available HELOC. Here’s how the interest calculation changes: Interest=50,000×0.07=3,500\text{Interest} = 50,000 \times 0.07 = 3,500With this smaller borrowing amount, you would pay $3,500 in interest annually. This scenario highlights one of the key benefits of a HELOC: you only pay interest on the amount you use. So, even though your HELOC is approved for up to $200,000, if you don’t use the full amount, you’re saving on interest.

Scenario 3: Borrowing the Full $200,000

Lastly, let’s imagine you decide to borrow the full $200,000 available in the HELOC. Here’s what the interest calculation looks like: Interest=200,000×0.07=14,000\text{Interest} = 200,000 \times 0.07 = 14,000In this scenario, you would pay $14,000 in interest each year. If you were in the draw period, and you only made interest-only payments, you would continue to pay this amount annually without reducing your principal. This is an important consideration when planning for future repayment obligations.

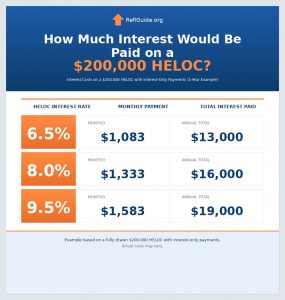

How Much Interest Would Be Paid on a $240,000 HELOC at 6.5%?

Calculating Interest on a $240,000 HELOC at 6.5%

When considering a $240,000 HELOC at an interest rate of 6%, the total amount of interest paid will depend on two main factors: how much of the credit line is used and how long you take to repay the borrowed amount. Since a Home Equity Line of Credit operates like a credit card, where you only pay interest on the funds you actually borrow, rather than the total available credit limit. Let’s explore how the HELOC interest would be calculated.

For example, if you were to borrow the full $240,000, you would calculate the interest by multiplying the borrowed amount by the interest rate. Using the formula:

Interest=Loan Amount×Interest Rate\text{Interest} = \text{Loan Amount} \times \text{Interest Rate}

In this case, the interest would be:

Interest=240,000×0.06=14,400\text{Interest} = 240,000 \times 0.06 = 14,400

This means you would pay $14,400 in interest per year if you borrow the full $240,000 and only make interest payments during the draw period. Keep in mind that many HELOCs allow interest-only payments during the initial draw period (typically 5 to 10 years), so if you don’t pay down the principal, you would continue to pay $14,400 annually. Over a 10-year draw period, for instance, you could pay $144,000 in interest if the entire amount remains borrowed without reducing the balance.

Now, suppose you only borrow a portion of the HELOC, say $120,000, the interest calculation would change significantly. The annual interest on $120,000 at 6% would be:

Interest=120,000×0.06=7,200\text{Interest} = 120,000 \times 0.06 = 7,200

This shows the key advantage of a HELOC: you only pay interest on the funds you use. Borrowing less saves you significant interest payments.

Why pay interest on money you don’t need when a HELOC allows you to borrow only what’s necessary and control your interest costs? This flexibility is one of the primary benefits of a HELOC, as it lets you manage your debt while keeping interest payments in check. By borrowing responsibly and paying down the principal over time, you can minimize the overall interest burden on your loan. Learn more about the current HELOC credit score requirements.

How Much Interest Would Be Paid on a $100,000 HELOC at 6%?

Calculating Interest on a $100,000 HELOC at 6%

When you take out a $100,000 HELOC at a 6% interest rate, the total interest paid will depend on how much you actually borrow from the line of credit and how long it takes you to repay the loan. Unlike traditional loans, where you receive the full amount upfront, a HELOC allows you to borrow funds as needed, meaning you only pay interest on the amount you use rather than the entire credit limit. But how much interest will you pay?

If you were to borrow the full $100,000 and only make interest payments during the draw period (the initial phase of the loan where you can access funds), the annual interest would be calculated as follows:

Interest=Loan Amount×Interest Rate\text{Interest} = \text{Loan Amount} \times \text{Interest Rate} Interest=100,000×0.06=6,000\text{Interest} = 100,000 \times 0.06 = 6,000

This means you would pay $6,000 in interest each year, assuming no principal is paid off during the draw period. If your HELOC has a draw period of 10 years, and you consistently borrowed the full $100,000 without making any principal payments, you could end up paying $60,000 in interest over that time.

However, the beauty of a HELOC lies in its flexibility. Suppose you only borrow $50,000 of the available credit. The interest for borrowing $50,000 at 6% would be:

Interest=50,000×0.06=3,000\text{Interest} = 50,000 \times 0.06 = 3,000

In this case, your annual interest payment would drop to $3,000, highlighting the advantage of borrowing only what you need.

Why pay interest on money you haven’t borrowed when a home equity line of credit lets you tap into funds as needed, saving you thousands in interest payments over time? This flexibility makes HELOCs a great option for those who want access to funds but don’t need to borrow the full amount upfront.

By using your home equity line of credit strategically and making payments on the principal when possible, you can reduce your interest burden and manage your finances more efficiently, tailoring your borrowing to fit your exact needs without paying unnecessary interest.

Factors Influencing HELOC Interest Costs

While these scenarios provide a snapshot of potential interest costs, several factors can influence how much you ultimately pay over the life of the HELOC:

How much you borrow: Since you only pay interest on the amount you actually borrow, careful planning about how much of your HELOC to use can significantly affect your interest costs. Borrowing only what’s necessary is a smart way to minimize interest payments.

Length of the draw period: During the draw period, you may only be required to make interest payments, but the longer this period lasts, the more interest you’ll accumulate. Making payments toward the principal during this time can reduce your overall interest costs in the long run. (Read more about how a HELOC compounds interest.)

Variable interest rates: Most HELOCs come with variable interest rates, meaning that the interest rate can fluctuate over time, depending on market conditions. If interest rates rise, you could end up paying more in interest, even if your principal remains the same. Conversely, if rates drop, your interest payments could decrease. It’s crucial to monitor rate changes and understand how they affect your payments.

A HELOC’s variable interest rate is like sailing on the open sea—sometimes the waters are calm, and other times, you’re navigating through choppy waves. Being prepared for these fluctuations is key to managing your loan effectively.

- Repayment period: Once the draw period ends, the repayment period begins, and you’ll start paying both principal and interest. The interest you pay during the repayment period will depend on the outstanding balance and the loan’s terms.

Strategies to Reduce HELOC Interest Payments

There are several ways you can minimize the amount of interest paid on a HELOC:

Borrow only what you need: Since you only pay interest on the amount borrowed, try to avoid using more of the credit line than necessary.

Make principal payments during the draw period: If your HELOC allows it, making payments toward the principal during the draw period can significantly reduce your overall interest costs. The smaller the principal, the less interest accrues over time.

Refinance or lock in a fixed rate: If your HELOC has a variable interest rate and you anticipate rising rates, consider refinancing the loan or converting it to a fixed-rate option. This can provide stability in your payments and help you avoid increasing interest costs in the future.

FAQ for HELOC and Interest

HELOC vs Home Equity Loan

The home equity loan is a simple interest lump-sum loan that has fixed monthly payment and fixed rates and terms for the life of the loan. The HELOC is a revolving line of credit that carries a variable interest rates. The HELOC is an open-end mortgage that includes an interest only payment option during the draw period.

How Is HELOC Interest Calculated?

During the draw period, HELOC interest is calculated on a daily basis by multiplying the daily balance by the daily interest rate. The daily interest rate is determined by dividing the annual interest rate by the number of days in the year. At the end of each billing cycle, the daily interest charges are summed to determine the monthly interest payment

How Long Does it Take to Get a Home Equity Loan?

On average a home equity loan or credit line takes 4 to 6 weeks to close. The RefiGuide will match you competitive lenders that can help you get an equity loan or HELOC in 2 weeks.

What Are the Closing Costs on HELOCs?

The closing costs range from 2 to 5% of the total credit line amount. If you took out a $50,000 HELOC and negotiated 2% in closing costs then you would be paying $1,000 in HELOC costs.

Can I Get Cash from a HELOC Line?

Yes, most banking companies and lending sources allow you to pull cash out directly from a home equity line of credit.

Takeaways on How Much Interest Is Paid with a HELOC

In summary, the amount of interest you pay on a $200,000 HELOC at 7% depends entirely on how much you borrow and for how long. Borrowing smaller amounts or paying down the principal sooner will help reduce your overall interest costs, while taking out the full amount will naturally lead to higher interest payments. As with any financial decision, it’s important to carefully plan your borrowing needs and repayment strategy to make the most of your HELOC.

Wouldn’t it be more beneficial to have a flexible loan option that grows with your needs while offering control over how much interest you pay? With a HELOC, that flexibility is precisely what you get.

About Bryan Dornan

Bryan Dornan is a marketing leader and financial journalist who currently serves as Chief Editor of RefiGuide.org. Bryan has founded several mortgage and digital marketing companies and has worked as a loan officer, mortgage broker and chief marketing officer in the industry for nearly 30 years and has a wealth of experience in providing mortgage clients with the highest level of service in the industry. Bryan's continual focus is to educate homeowners how to leverage home equity while also promoting affordable home-ownership to consumers like you across the United States. He also writes for RealtyTimes, Patch, Buzzfeed, Medium and other national publications. Find him on Twitter, Muckrack, and Linkedin

More articles by Bryan Dornan